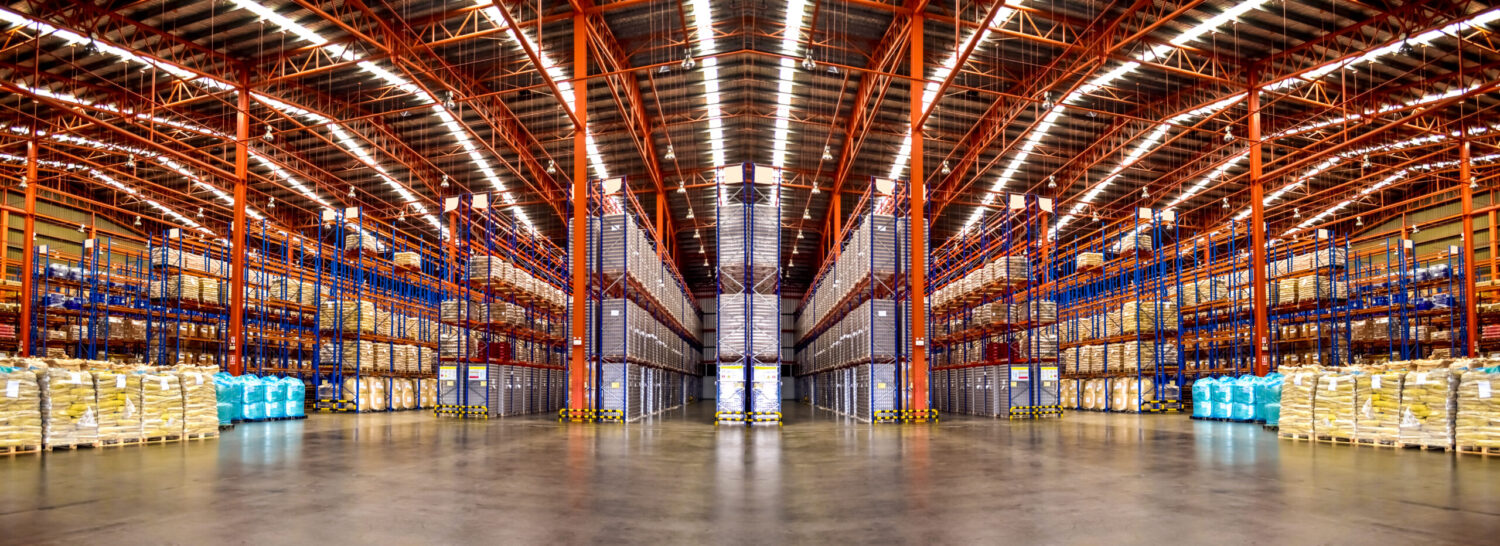

What is Inventory Management?

Inventory management is a critical aspect of effective supply chain management strategies, involving the supervision of non-capitalized assets and stock items. This process ensures that the right quantity and quality of inventory are maintained to meet business needs while minimizing storage and holding costs. It comprises tracking, controlling, and managing goods from manufacturers to warehouses and from these facilities to point of sale, often incorporating lean inventory management principles.

By better managing your inventory you will better manage your money. Poor inventory management leads to too much money tied up in needless inventory, or unsatisfied customers upset at missed deliveries.

Inventory Management Strategy vs Tactics

Understanding the difference between strategy and tactics is pivotal to effective inventory management. Strategy refers to the broader, long-term goals that set the direction for an organization, often encompassing distribution strategies in supply chain management and global supply chain management strategy. In contrast, tactics are specific, short-term actions or approaches used to achieve these strategies, such as implementing an inventory barcode system or choosing the right ERP system for manufacturing.

Inventory Management Strategies

Navigating the complex terrain of inventory management requires the application of carefully curated strategies. Each of the sample strategies here corresponds to unique operational preferences and market environments, affecting the production, storage, and delivery of inventory.

Push Strategy

The push strategy, in the realm of inventory management, is a forward-thinking methodology that bases production on anticipated demand. Companies implement this strategy by manufacturing and storing goods in advance, relying on demand forecasts to drive production schedules. This proactive approach ensures a steady flow of goods ready for dispatch, effectively catering to markets with predictable consumption patterns.

However, the push strategy isn’t without its potential drawbacks. While it shines in a predictable market, inaccuracies in demand forecasting can lead to costly overstocks or, conversely, stock shortages. The effectiveness of this strategy hinges heavily on the accuracy of demand prediction models and understanding consumer behavior.

Pull Strategy

Opposite the push strategy is the pull strategy. Here, production is driven by actual, rather than anticipated, customer demand. This means that companies only manufacture goods when an order has been placed, effectively eliminating the risk of excessive inventory.

Despite its advantages, the pull strategy necessitates a highly agile and responsive production process. If customer demand suddenly surges, a company must be able to rapidly increase production to prevent delivery delays. Therefore, while this strategy minimizes stock holding costs, it requires a highly flexible operational framework to respond to demand variations effectively.

Just in Time Strategy

The Just in Time (JIT) strategy is a hybrid approach combining aspects of both push and pull strategies. JIT is rooted in lean inventory management principles, aiming to reduce waste by synchronizing production schedules with actual demand, thereby ensuring goods are produced precisely when needed.

While JIT offers several benefits, including reduced inventory costs and improved efficiency, it also presents certain challenges. It requires highly accurate demand forecasting and a well-oiled supply chain, as any delays in production or delivery can cause significant disruptions. Moreover, a JIT approach offers little room for error or unexpected changes in demand, making it a less suitable choice for markets prone to volatility or unpredictability.

Inventory Management Tactics

While strategies set the general direction for inventory management, tactics are the day-to-day actions that bring these strategies to life. These tactical decisions revolve around specific practices and tools that optimize operations and contribute to the overarching goal of effective inventory management.

Get and keep accurate inventory

Maintaining accurate inventory records is a fundamental aspect of inventory management. Small companies might initially manage this visually, but as operations expand, the need for a more sophisticated approach emerges. Centralizing data in an ERP system becomes essential, offering not only accurate inventory tracking but also integration with other business processes. The benefits of ERP in supply chain management include real-time inventory updates, reduced human error, and improved operational efficiency.

Track and Manage Expiry Dates

Managing expiry dates is a critical concern, especially for businesses dealing with perishable goods. Expired inventory represents a significant cost and can lead to loss of sales and potential damage to the brand reputation. Implementing practices like First-Expiry-First-Out (FEFO) and First-In-First-Out (FIFO) can help manage and reduce the risk of expired stock. Ensuring staff know what to pick and where to pick it from helps ensure you aren’t wasting money on inventory that spoils too soon.

Increase visibility in the warehouse with scanners

Enhancing warehouse visibility is another essential tactic in inventory management. The introduction of a barcode management system can drastically improve the speed and accuracy of inventory tracking. Inventory barcode systems allow immediate identification, location, and tracking of inventory items, providing a real-time snapshot of stock levels and aiding in the efficient management of warehouse operations. An ERP can then guide picking and packing operations for staff based on the days production and shipping schedules.

Automate demand planning

Automating demand planning is a progressive step towards achieving a lean inventory. This involves utilizing advanced ERP systems, predictive analytics, and AI to anticipate future demand based on historical data and market trends. Automated demand planning not only improves forecast accuracy but also enables timely inventory replenishment and reduces stockouts or overstock scenarios.

Set reorder points

Establishing reorder points is a practical approach to ensure inventory availability while minimizing stockholding costs. This involves determining a threshold at which new stock should be ordered, considering factors such as lead time, demand rate, and safety stock. Reorder points act as a trigger for replenishment, ensuring a steady supply of inventory and aligning with the ‘just in time’ strategy in supply chain management.

Inventory Management

Inventory management remains a cornerstone of successful supply chain operations. By employing strategic approaches and tactical measures, businesses can enhance efficiency, reduce costs, and meet customer demands effectively. Remember, no single strategy or tactic is one-size-fits-all; instead, the optimal inventory management approach varies according to business size, industry, and specific operational needs. It’s all about finding the right blend of push and pull strategies, incorporating lean inventory management principles, and harnessing the power of modern tools like ERP systems and barcode scanners.

The world of inventory management is ever-evolving, with new strategies, technologies, and best practices emerging regularly. Staying informed is key to maintaining a competitive edge. To keep up with the latest trends and insights in inventory management and supply chain strategy, subscribe to our newsletter. We deliver valuable content right to your inbox, helping you stay ahead of the curve in this dynamic industry. Join us on this journey.